In early 2026, carbon prices under the European Union’s Emissions Trading System (EU ETS) surged sharply, marking one of the most decisive price escalations in the system’s history and signalling a new, more restrictive phase of EU climate policy.

This acceleration was driven by a convergence of structural supply tightening, regulatory reform, and the effective rollout of the Carbon Border Adjustment Mechanism (CBAM), which together reinforced the credibility and the cost of the EU’s decarbonisation agenda. While higher carbon prices strengthen investment signals for low-carbon technologies and confirm the EU ETS as the central pillar of European climate governance, they also translate into immediate and tangible economic pressures for industrial actors, particularly in energy-intensive sectors.

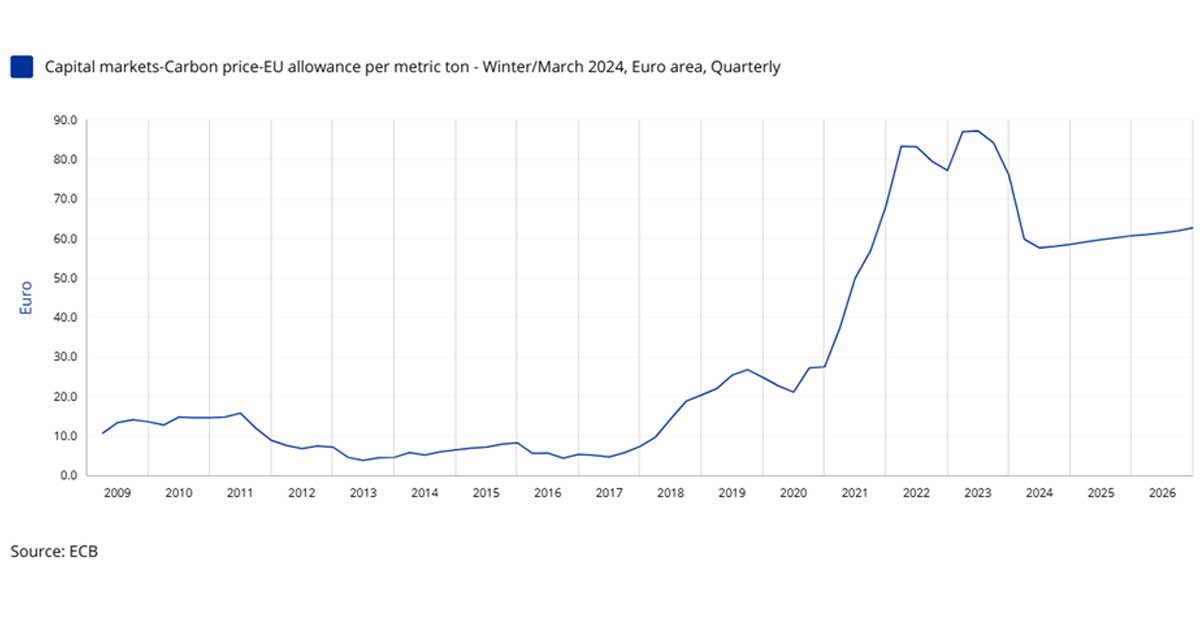

As a market-based mechanism covering more than 40% of EU greenhouse gas emissions, the EU ETS internalises the cost of carbon through a declining emissions cap and tradable allowances, with successive reforms steadily constraining supply and elevating prices. By late 2025 and early 2026, this tightening was clearly reflected in the market: analysts projected average EUA prices of €83-92 per tonne of CO₂ for 2026, up from roughly €75 in 2025, with some forecasts anticipating temporary spikes above €100 per tonne in early 2026. These expectations were reinforced by stronger hedging demand from compliance entities and heightened regulatory certainty linked to CBAM implementation.

For Hungary, where steel, cement, power generation and chemical industries remain central to economic performance and employment, rising carbon prices represent a concrete cost factor shaping operational strategies, investment planning and international competitiveness. Deep integration into European value chains means that shifts in EU carbon pricing directly affect compliance burdens, export conditions and long-term decarbonisation choices. Against this backdrop, this analysis examines the drivers behind the early-2026 surge in EU carbon prices, reviews prevailing market forecasts, and assesses their implications for Hungarian industry, with the objective of informing pragmatic, evidence-based policymaking and corporate decision-making.

Price Movements and Forecasts

Carbon prices under the EU ETS moved decisively higher in the second half of 2025, culminating in a sharp rally in December. By year-end, EU Allowance (EUA) prices reached their highest level in nearly two years, with the December 2026 futures contract exceeding €87 per tonne of CO₂ and spot prices consistently trading above €80 per tonne. This marked a clear break from the temporary stabilisation seen earlier in 2025, when weaker industrial activity and lower gas prices had briefly eased carbon market pressures.

Market expectations strongly reinforced this upward momentum into 2026. Montel projected an average EUA price of around €92.02 per tonne for 2026, nearly 24% higher than the estimated 2025 average. More cautious forecasts, including those from ING, still pointed to elevated levels, with averages of roughly €83 per tonne in 2026 versus €75 per tonne in 2025. Several scenario analyses further indicated that prices could temporarily exceed €100 per tonne, particularly in early 2026, when compliance-related hedging typically peaks. The futures curve itself shifted into backwardation in late 2025, signalling near-term scarcity and growing confidence that ETS tightening is durable rather than cyclical.

Market expectations strongly reinforced this upward momentum into 2026. Montel projected an average EUA price of around €92.02 per tonne for 2026, nearly 24% higher than the estimated 2025 average. More cautious forecasts, including those from ING, still pointed to elevated levels, with averages of roughly €83 per tonne in 2026 versus €75 per tonne in 2025. Several scenario analyses further indicated that prices could temporarily exceed €100 per tonne, particularly in early 2026, when compliance-related hedging typically peaks. The futures curve itself shifted into backwardation in late 2025, signalling near-term scarcity and growing confidence that ETS tightening is durable rather than cyclical.

Market Mechanics: Reduced Allowance Supply

The dominant driver behind rising prices is the progressive tightening of allowance supply under the reformed EU ETS. The Market Stability Reserve continues to withdraw and cancel surplus allowances, materially reducing market liquidity and preventing a return to oversupply. At the same time, Fit for 55 reforms are accelerating the decline in free allocations, while the gradual phase-out of free allowances in aviation adds further pressure on demand for auctioned EUAs. Auction volumes are also set to fall sharply: some estimates suggest a 25-30% reduction in 2026 compared with earlier years, significantly increasing price sensitivity during compliance periods. As a result, the ETS has shifted from a surplus-driven system to one defined by structural scarcity, where even modest demand increases can trigger strong price reactions.

Speculative and Financial Market Dynamics

Financial market behaviour has amplified these trends. In late 2025, investment funds moved decisively from net short to net long positions in EUA futures, coinciding with a price increase of over 30% within six weeks. Unlike earlier phases of the ETS, this speculative activity appears closely aligned with long-term policy fundamentals, reinforcing rather than undermining price signals. While greater financial participation has increased liquidity and sharpened short-term volatility during periods of geopolitical and energy-market uncertainty, the persistence of high prices into early 2026 confirms that financial flows are operating within a structurally tightening carbon market.

Full Implementation of the Carbon Border Adjustment Mechanism

A major policy shift effective from 1 January 2026 was the full implementation of the EU Carbon Border Adjustment Mechanism (CBAM). CBAM imposes a carbon price on imports of selected carbon-intensive goods (steel, cement, fertilisers, aluminium and electricity) based on their embedded emissions. It replaces certain aspects of free allocation under the ETS and seeks to prevent carbon leakage, were production moves to jurisdictions with less stringent climate policies.

CBAM’s implementation increases demand for EUAs due to the anticipated compliance requirements and hedging demand by importers. The mechanism’s broader effects on global trade energy costs are substantial: CBAM exposure is not limited to local producers but affects exporters worldwide, including from countries such as Turkey or China whose exports to the EU are carbon intensive.

ETS Allowance Reforms and Cap Reductions

Alongside the implementation of the Carbon Border Adjustment Mechanism, the European Union has enacted substantial reforms to the core architecture of the EU Emissions Trading System under the Fit for 55 legislative frameworks. These reforms are designed to align the ETS with the EU’s strengthened climate objectives, notably the legally binding target of reducing net greenhouse gas emissions by at least 55% by 2030 relative to 1990 levels.

A key component of these reforms is the acceleration of the linear reduction factor, which determines the annual decline in the overall emissions cap. The revised cap trajectory results in a steeper and more predictable contraction of allowance supply compared to previous ETS phases, reinforcing long-term scarcity. In parallel, benchmark values used for free allocation have been revised downward to reflect more ambitious efficiency standards, thereby reducing the volume of allowances allocated at no cost and increasing reliance on auctioned allowances.

Further tightening has resulted from reforms to the Market Stability Reserve, including strengthened intake thresholds and provisions for the permanent cancellation of surplus allowances. Together, these measures have significantly reduced the effective supply buffer within the system, increasing price sensitivity to changes in demand and regulatory expectations. As a result, market participants increasingly perceive allowance scarcity as both credible and durable, contributing to elevated price expectations into 2026 and beyond.

Macro-Economic and Industrial Drivers: Decoupling from Energy Commodity Prices

Historically, EU carbon prices moved closely in line with fossil energy markets, especially natural gas, as fuel-switching in power generation largely determined short-term allowance demand. Higher gas prices increased the marginal cost of gas-fired electricity, pushing up EUA demand and prices, while cheaper gas typically eased carbon market pressures. However, from 2024 onward (and more clearly through 2025 and early 2026) this relationship weakened. Despite softer gas prices driven by improved supply and lower demand, EU ETS prices continued to rise, signalling a structural decoupling rooted in regulatory reform rather than energy commodity dynamics. As the emissions cap tightens and surplus allowances are cancelled, carbon prices have become increasingly anchored to expectations of long-term scarcity, functioning more as a forward-looking policy signal than a reflection of short-term fuel price movements.

Industrial Demand and Hedging Behaviour

At the same time, industrial demand has become more structural. Power producers and energy-intensive industries have shifted toward active carbon risk management, increasingly hedging future compliance obligations through forward and futures markets rather than relying on spot purchases. Rising price expectations and clearer regulatory trajectories under the reformed ETS encourage firms to secure allowances earlier, smoothing costs but sustaining demand in carbon markets. Unlike earlier ETS phases, this hedging activity is now less cyclical and more driven by compliance certainty and long-term investment planning, amplifying upward price pressure in an environment of declining auction volumes and tighter liquidity.

Global Energy Market Context

While global energy markets continue to influence industrial output and power generation indirectly, the EU ETS has increasingly diverged from oil and gas price cycles. Entering 2026, global energy markets were marked by volatility and uncertainty, conditions that previously might have dampened carbon prices. Instead, EUA prices remained elevated, reflecting the dominance of regulatory design, allowance scarcity and compliance-driven demand. This growing autonomy underscores the transformation of carbon pricing into an independent economic factor, increasingly shaped by policy credibility and long-term emissions targets. For industry, this means carbon costs are no longer a secondary variable, but a central and persistent element shaping production, investment and competitiveness decisions.

Implications for Hungarian Industry

Hungary’s economic strength rests on a robust, export-oriented manufacturing base, spanning steel, chemicals, energy generation, automotive supply chains and cement, and therefore the tightening of EU carbon pricing has clear strategic significance. Unlike service-driven economies, Hungarian competitiveness depends on affordable energy, supply security and predictable investment conditions, all of which the government consistently treats as matters of economic sovereignty and employment protection. Rising carbon prices must therefore be assessed not only as a climate policy instrument, but as a factor shaping national industrial resilience and long-term growth.

Under the reformed EU ETS, higher EUA prices inevitably increase compliance costs for Hungarian industrial producers. While transitional safeguards and free allocations continue to shield leakage-exposed sectors, their gradual phase-out places growing pressure on domestic firms. This is particularly relevant in a Single Market where Western European competitors often benefit from stronger capital positions, earlier access to subsidised green finance and structurally lower energy intensity. Hungarian companies are thus required to adjust to carbon pricing while also managing energy market volatility stemming from Europe’s accelerated energy transition. The introduction of CBAM, though justified in principle as a defensive trade instrument, adds further administrative and cost burdens, which may weigh disproportionately on export-oriented Hungarian manufacturers and SMEs embedded in multinational value chains.

At the same time, the government recognises that carbon pricing can be used strategically to support industrial modernisation rather than industrial decline. Targeted investments in energy efficiency, selective electrification, renewable integration and (where economically justified) carbon capture technologies offer pathways to reduce long-term cost exposure without sacrificing production capacity. From a conservative and pragmatic policy perspective, decarbonisation must remain gradual, technologically neutral and investment-led, focused on safeguarding jobs, strengthening energy security and preserving Hungary’s role as a competitive manufacturing hub. Well-coordinated decarbonisation efforts can enhance resilience, reduce import dependence and reinforce national strategic autonomy.

Finally, as CBAM reshapes trade conditions, Hungary’s deep integration into European value chains requires proactive engagement with suppliers and partners to maintain export competitiveness. At the same time, the government has a clear interest in ensuring that CBAM implementation remains proportionate and administratively manageable, reflecting Central European industrial realities. In this context, Hungary’s policy approach, centred on realism, national interest and continuous dialogue with industry, provides a stable framework for navigating rising carbon prices while defending economic growth, regional development and long-term industrial strength.

Conclusion

The sharp rise in EU carbon prices in early 2026 is not a temporary market anomaly but the result of a fundamental transformation of the EU ETS into a scarcity-driven, policy-anchored system. Structural supply tightening, the full implementation of CBAM, accelerated cap reductions and increasingly forward-looking market behaviour have combined to lock in higher and more persistent carbon prices. In this environment, carbon pricing has evolved from a secondary cost factor into a central economic variable, shaping industrial strategy, investment horizons and trade competitiveness across the Union.

For Hungary, higher compliance costs will gradually increase the adjustment needs of energy-intensive sectors, particularly in areas with higher capital and energy exposure, while competitive conditions within the Single Market may become more demanding. At the same time, the greater predictability of the evolving carbon regime provides Hungarian industry with a clearer and more stable framework for long-term planning, technological modernisation and carbon risk management, especially if policy responses continue to be pragmatic and firmly aligned with national economic interests.

The central question is therefore not whether carbon prices will remain elevated, but how Hungary can best adapt to and shape this evolving regulatory environment. A gradual, technologically neutral and investment-led transition, underpinned by energy security, targeted industrial support and constructive engagement at EU level, offers the opportunity to transform regulatory change into a driver of industrial resilience and long-term competitiveness. In this context, the early-2026 carbon price surge highlights the growing alignment between climate and industrial policy, reinforcing the importance of realistic planning, strategic foresight and continuous cooperation between government and industry.

References

European Commission. (2023). Fit for 55: Delivering the EU’s 2030 Climate Target on the Way to Climate Neutrality. Publications Office of the European Union.

European Parliament & Council of the European Union. (2021). Directive (EU) 2018/410 on the reduction of greenhouse gas emissions and the functioning of the EU Emissions Trading System (ETS).

International Energy Agency. (2025). Market dynamics and carbon pricing in the EU. IEA Publications.

Montel Market Insight. (2026). EU ETS price forecasts and market dynamics. Montel Analytics.

Schneider, L., & La Hoz Theuer, S. (2019). Price and market dynamics in emissions trading systems: A review of empirical evidence. Business Strategy and the Environment, 28(7), 1330–1347.

Smekalova, T., & Kocmanová, A. (2024). Decarbonisation pathways in industrial policy within EU frameworks. In S. D. Authors (Ed.), European Industrial Transformation (pp. 145–162). Springer.

World Bank. (2025). State and trends of carbon pricing 2025. World Bank Publications.

Aldy, J. E., & Stavins, R. N. (2012). The promise and problems of pricing carbon: Theory and experience. Journal of Environment & Development, 21(2), 152–180.

Böhringer, C., & Lange, A. (2005). Economic impacts of the EU emissions trading scheme: A multi-sector CGE assessment. Energy Economics, 27(3), 297–317.

Ellerman, A. D., Joskow, P. L., Schmalensee, R., Montero, J. P., & Bailey, E. M. (2016). Markets for clean air: The US acid rain program. Cambridge University Press.

Fabra, N., & Reguant, M. (2014). Pass-through of emissions costs in electricity markets. American Economic Review, 104(9), 2872–2899.

Helm, D. (2005). Economic instruments and environmental policy. Oxford University Press.

Hintermann, B., Peterson, S., & Rickels, W. (2016). Price discovery in the European carbon market. Journal of Environmental Economics and Management, 78, 121–145.

Pahle, M., Burtraw, D., & Flachsland, C. (2018). The European Union Emissions Trading System and the global carbon market. Climate Policy, 18(5), 611–624.

Perino, G., & Willner, M. (2016). Price dynamics in the EU ETS. Energy Economics, 56, 548–556.

Sijm, J., Neuhoff, K., & Chen, Y. (2006). CO₂ cost pass-through and electricity prices: Evidence from the European power market. Energy Economics, 28(1), 1–16.

Trotignon, R., & Delbosc, A. (2020). Carbon border adjustments: Design, impact, and industrial strategy. Climate Policy, 20(9), 1100–1116.

Weber, C., & Neuhoff, K. (2010). Climate policy and industrial competitiveness: Impacts and policy options. Climate Policy, 10(6), 585–608.

Zetterberg, L. (2022). Hedging strategies and market behaviour in the EU ETS: Evidence from 2018–2021. Energy Policy, 167, 113045.