Over the past decade, environmental, social, and governance (ESG) principles have rapidly moved from the margins of corporate strategy to the centre of economic governance across the European Union. Sustainability reporting, climate commitments, and responsible investment have become essential elements of corporate reputation, financial market performance, and regulatory oversight. However, the rapid institutionalization of ESG frameworks has also generated a serious credibility deficit. The widespread phenomenon of greenwashing, the practice of exaggerating, misrepresenting, or fabricating sustainability claims, has undermined consumer trust, distorted investment decisions, and weakened the legitimacy of climate policy.

According to studies commissioned by the European Commission, more than half of corporate environmental claims within the EU are either vague, misleading, or unsupported by credible evidence, while nearly 40 percent lack any form of substantiation. This reality exposes fundamental weaknesses in the EU’s sustainability governance model and highlights the risks of relying on voluntary disclosure and self-regulation. As a result, the European Union has initiated one of the most ambitious regulatory reforms in the field of sustainability reporting and consumer protection, aimed at eliminating greenwashing and restoring market credibility.

By 2026, a comprehensive legislative framework built around the Corporate Sustainability Reporting Directive (CSRD), the European Sustainability Reporting Standards (ESRS), and the Empowering Consumers for the Green Transition Directive will fully enter into force. This regulatory architecture will significantly reshape corporate disclosure obligations, environmental marketing practices, and financial supervision mechanisms. While the reform seeks to strengthen transparency and accountability, it also raises critical questions about regulatory burden, economic competitiveness, national sovereignty, and administrative feasibility, particularly for medium-sized economies such as Hungary.

This article examines the political logic, regulatory structure, economic implications, and national consequences of the EU’s greenwashing crackdown, with particular emphasis on Hungary’s strategic interests, industrial structure, and economic resilience.

The Strategic Logic Behind the EU’s Regulatory Overhaul

The EU’s greenwashing crackdown is embedded within a broader transformation of European economic governance under the framework of the European Green Deal. Sustainability has been elevated from a policy objective to a guiding principle shaping industrial strategy, financial regulation, and market oversight. In this context, ESG reporting is increasingly treated as an instrument for steering capital flows, restructuring industrial production, and achieving climate neutrality.

From Brussels’ perspective, eliminating greenwashing is essential to safeguarding the credibility of sustainable finance and preventing the misallocation of capital. Investors require reliable and comparable ESG data to price risk accurately, while consumers must be protected from deceptive marketing practices. At the same time, the regulatory approach reflects a broader ideological shift toward centralized standard-setting and harmonized compliance mechanisms.

However, this centralization also generates legitimate concerns among member states. Excessive regulatory density risks undermining national economic flexibility, imposing disproportionate administrative burdens on domestic enterprises, and weakening industrial competitiveness. For countries such as Hungary, whose economic growth is heavily dependent on manufacturing exports, foreign direct investment, and integration into global supply chains, regulatory overreach poses tangible strategic risks.

The Greenwashing Directive: Recalibrating Environmental Marketing

The Empowering Consumers for the Green Transition Directive, which will apply fully from September 2026, introduces strict limitations on corporate environmental claims. Generic descriptors such as “eco-friendly,” “sustainable,” or “climate neutral” will be prohibited unless supported by rigorous scientific evidence. Claims based exclusively on carbon offsetting schemes will also face severe restrictions.

The directive effectively transforms environmental marketing into a regulated compliance domain. Companies must maintain verifiable documentation, conduct life-cycle assessments, and subject sustainability claims to external scrutiny. While this strengthens consumer protection and reduces deceptive practices, it also introduces substantial legal and administrative complexity.

For Hungarian enterprises, particularly in sectors such as food processing, tourism, logistics, and energy services, these changes require a fundamental rethinking of communication strategies. Compliance costs will increase, while legal risks associated with misrepresentation will intensify. However, companies that successfully adapt may gain reputational advantages in EU markets increasingly shaped by sustainability-driven consumer behaviour.

CSRD and ESG Reporting: Structural Transformation of Corporate Governance

The Corporate Sustainability Reporting Directive represents the most far-reaching element of the EU’s regulatory package. By expanding mandatory ESG reporting obligations to over 50,000 firms, including large enterprises and listed SMEs, CSRD introduces a new paradigm of corporate accountability.

Companies must disclose detailed information on climate risks, emissions, biodiversity impacts, labour practices, governance structures, and supply-chain sustainability. These disclosures must follow standardized European Sustainability Reporting Standards and undergo independent external verification. The introduction of mandatory auditing effectively elevates ESG data to the same legal status as financial statements.

The principle of double materiality further expands corporate responsibility by requiring firms to report not only how sustainability issues affect financial performance but also on how corporate activities impact society and the environment. While conceptually coherent, this framework significantly increases compliance complexity, particularly for manufacturing-heavy economies such as Hungary’s.

The Omnibus Simplification: Recalibrating Scope and Timeline

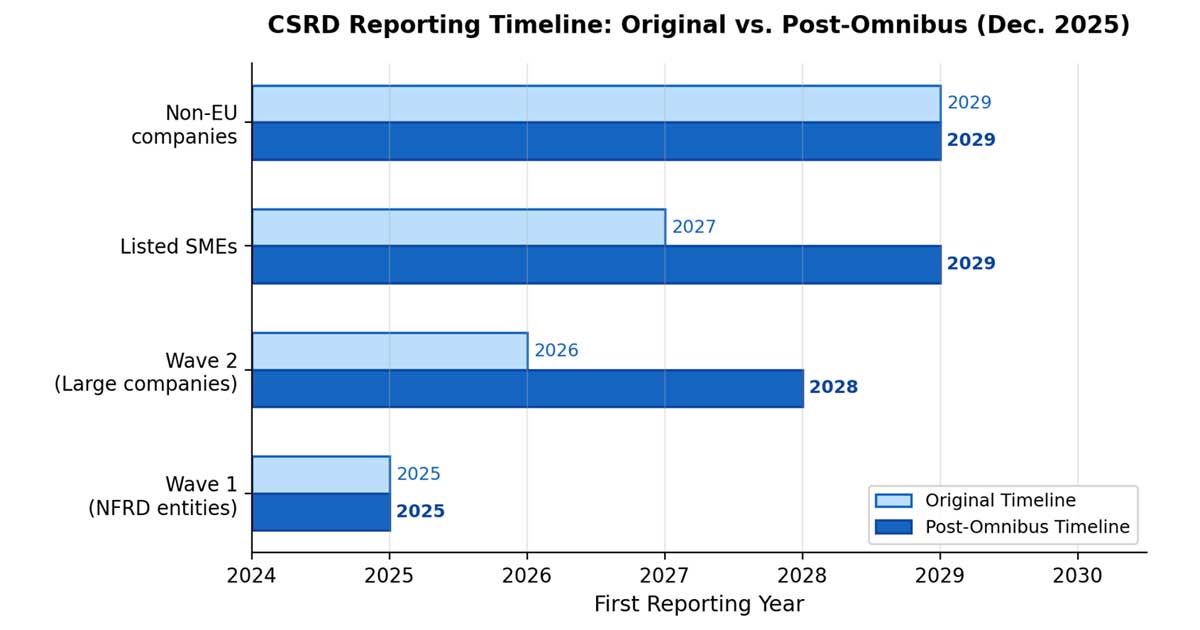

Mounting concerns over regulatory overload prompted the European Commission to adopt the Omnibus I simplification package on 26 February 2025. This legislative intervention represents a significant recalibration of the CSRD’s ambition, triggered by sustained political pressure from member states and business associations demanding relief from compliance complexity. The so-called “Stop-the-Clock” directive, published in the Official Journal on 16 April 2025, immediately postponed by two years the reporting obligations for Wave 2 and Wave 3 companies that had not yet begun reporting.

The substantive Omnibus I agreement, reached provisionally between the European Parliament and the Council on 9 December 2025, narrowed the CSRD’s mandatory scope to EU companies with more than 1,000 employees and more than €450 million in net annual turnover, a substantial departure from the original “two-out-of-three” threshold test that had captured a far broader range of enterprises. The agreement simultaneously raised the CSDDD thresholds to 5,000 employees and €1.5 billion in turnover. According to the European Commission’s own impact assessment, these modifications are expected to reduce administrative costs by approximately €4.4 billion annually across the EU, with one-off savings for newly exempted firms projected at around €1.6 billion.

Figure 1. CSRD reporting timeline comparison: original schedule versus post-Omnibus revisions (December 2025). Source: Compiled from European Commission, Council, and Parliament legislative documents.

Figure 1. CSRD reporting timeline comparison: original schedule versus post-Omnibus revisions (December 2025). Source: Compiled from European Commission, Council, and Parliament legislative documents.

For Hungary, the Omnibus revisions carry particular significance. As GKI Economic Research Institute has noted, large Hungarian companies that were originally expected to begin CSRD reporting in 2026 will now face a 2028 deadline, reporting on 2027 financial year data. This reprieve provides a critical adjustment window. However, GKI’s analysis also emphasizes that the postponement should not be misinterpreted as an abolition of obligations. Supply-chain pressures from multinational partners already demanding ESG data from Hungarian suppliers will continue to intensify regardless of formal regulatory timelines, making early preparation strategically essential.

Hungary was among the first EU member states to transpose the CSRD into national law, demonstrating proactive regulatory engagement. Nevertheless, Hungary’s domestic ESG legislation will need to be updated to reflect the revised Omnibus thresholds before the December 2025 transposition deadline set by the EU . This legislative agility positions Hungary to shape implementation in ways that balance compliance with national economic priorities.

Economic and Strategic Implications for Hungary

For Hungary, the EU’s greenwashing crackdown creates a complex mix of risks and opportunities. On the one hand, increased regulatory requirements impose substantial compliance costs, administrative burdens, and reporting obligations. On the other hand, improved transparency can strengthen investor confidence, facilitate access to sustainable finance, and enhance the long-term competitiveness of the Hungarian economy.

Large Hungarian enterprises and subsidiaries of multinational corporations will face immediate obligations under CSRD. This will necessitate investments in data infrastructure, sustainability expertise, compliance systems, and internal governance reforms. While multinational groups may absorb these costs more easily, domestically owned firms face significantly higher adjustment pressures.

Small and medium-sized enterprises, which form the backbone of the Hungarian economy, are formally exempt from many CSRD requirements. However, indirect compliance obligations will increasingly arise through supply-chain pressures. Multinational buyers and Western European partners will demand ESG data from Hungarian suppliers, effectively extending regulatory compliance throughout industrial ecosystems. Without targeted policy support, these dynamic risks create competitive asymmetries and regulatory fragmentation.

From a strategic perspective, Hungary must pursue a pragmatic regulatory adaptation strategy that prioritizes economic competitiveness, administrative efficiency, and technological modernization. Rather than resisting EU regulation outright, the government can leverage compliance requirements to promote digitalization, industrial upgrading, and energy efficiency investments.

Sovereignty, Competitiveness, and Regulatory Balance

The EU’s sustainability governance framework raises fundamental questions about regulatory sovereignty and economic self-determination. Centralized ESG standards, while promoting harmonization, limit national discretion in economic policymaking. For Hungary, maintaining regulatory autonomy in key industrial and energy sectors remains strategically essential.

A balanced approach requires assertive representation of national interests in EU negotiations, continuous evaluation of regulatory proportionality, and strategic use of available flexibility mechanisms. Hungary should advocate for simplified reporting regimes for SMEs, extended transition periods for high-emission industries, and targeted EU financial support for regulatory adaptation.

At the same time, alignment with EU sustainability standards offers long-term benefits. Global capital markets increasingly prioritize ESG-compliant investment destinations. Regulatory credibility enhances Hungary’s attractiveness for foreign investors, particularly in advanced manufacturing, automotive innovation, and clean energy technologies.

Financial Sector Implications

The greenwashing crackdown will significantly reshape Hungary’s financial ecosystem. Banks, investment funds, and insurers will face heightened ESG disclosure obligations, stricter risk assessment frameworks, and increased supervisory scrutiny. While this raises compliance costs, it also enhances financial stability by improving risk pricing and long-term capital allocation efficiency.

Hungary’s banking sector can benefit from the expansion of green lending instruments, sustainability-linked loans, and climate-focused investment products. Strategic alignment between regulatory adaptation and financial innovation could position Hungary as a regional leader in sustainable finance, strengthening Budapest’s role as a Central European financial hub.

Hungary’s Green Finance Leadership: The Role of the MNB and ÁKK

While the EU’s regulatory framework imposes new compliance demands, Hungary has proactively positioned itself as a regional frontrunner in green finance through the pioneering efforts of the Magyar Nemzeti Bank (MNB) and the Government Debt Management Agency (Államadósság Kezelő Központ, ÁKK). These institutional achievements provide a substantial foundation upon which Hungary’s ESG transition can build, transforming regulatory obligation into competitive advantage.

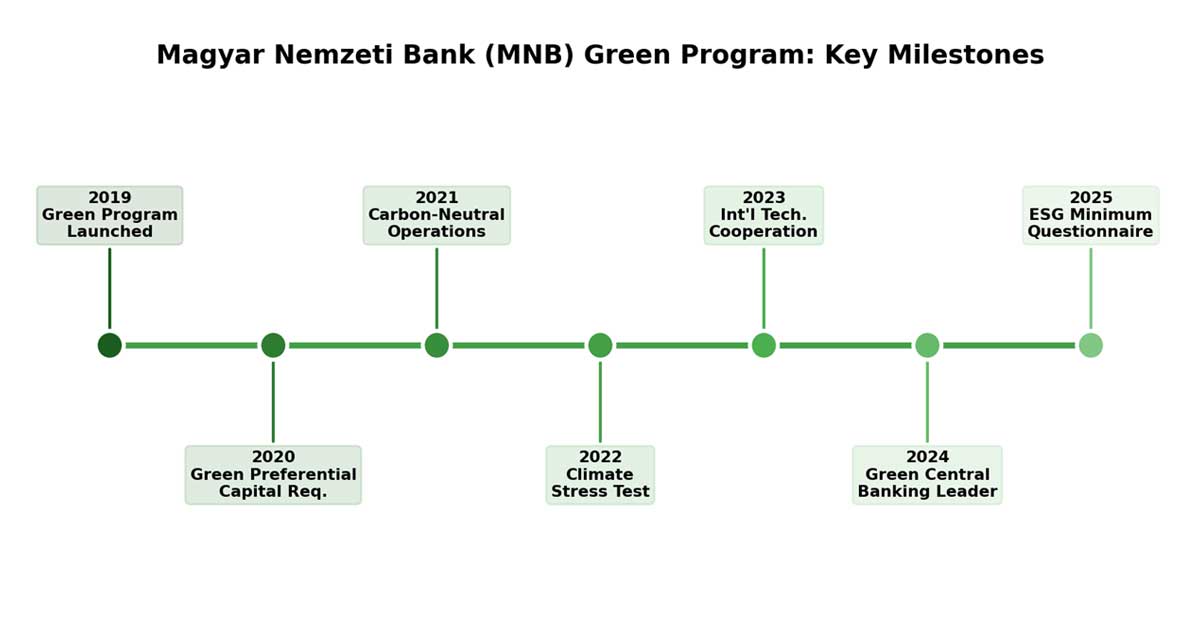

The MNB’s Green Program: A Comprehensive Central Bank Strategy

The MNB launched its Green Program in early 2019, establishing one of the most comprehensive central bank sustainability frameworks in Europe. The program operates across three strategic pillars: strengthening the resilience of the financial system against climate risks, developing green financing instruments and markets, and reducing the ecological footprint of the central bank’s own operations. In 2021, the MNB’s mandate was formally expanded to include supporting the government’s policy on environmental sustainability, providing a legal basis for integrating green objectives into monetary and supervisory policy.

Figure 2. Key milestones in the MNB’s Green Program (2019–2025). Source: Compiled from Magyar Nemzeti Bank publications and press releases.

Figure 2. Key milestones in the MNB’s Green Program (2019–2025). Source: Compiled from Magyar Nemzeti Bank publications and press releases.

A particularly innovative instrument is the MNB’s Green Preferential Capital Requirement Programme, introduced in 2019 for housing loans and extended in 2021 to corporate and municipal financing. Under this scheme, banks receive a capital requirement discount of 5 to 7 percent on eligible green exposures, incentivizing lending toward energy-efficient construction, renewable energy, and environmentally sustainable municipal investments. A 2024 evaluation published in the Financial and Economic Review found that the programmes generated measurable market development impacts across the banking system while reducing aggregate capital requirements by a modest 0.31 percentage points, confirming their prudential soundness. In light of these positive results, the programmes have been extended for a uniform period of time.

The MNB has also achieved carbon-neutral operations since 2021, surpassing its own targets. Its original goal of a 30 percent reduction in operational carbon footprint by 2022 was exceeded with a 60 percent reduction, prompting a revised target of 75 percent by 2025. In an independent assessment using the Green Central Banking Scorecard methodology, validated by Positive Money, the MNB scored higher than any G20 central bank on green monetary and financial policy metrics, underscoring the institution’s international leadership. Furthermore, in June 2025, the MNB issued Recommendation No. 7/2025 on the application of a minimum ESG questionnaire in credit risk assessment, further embedding sustainability considerations into prudential supervision.

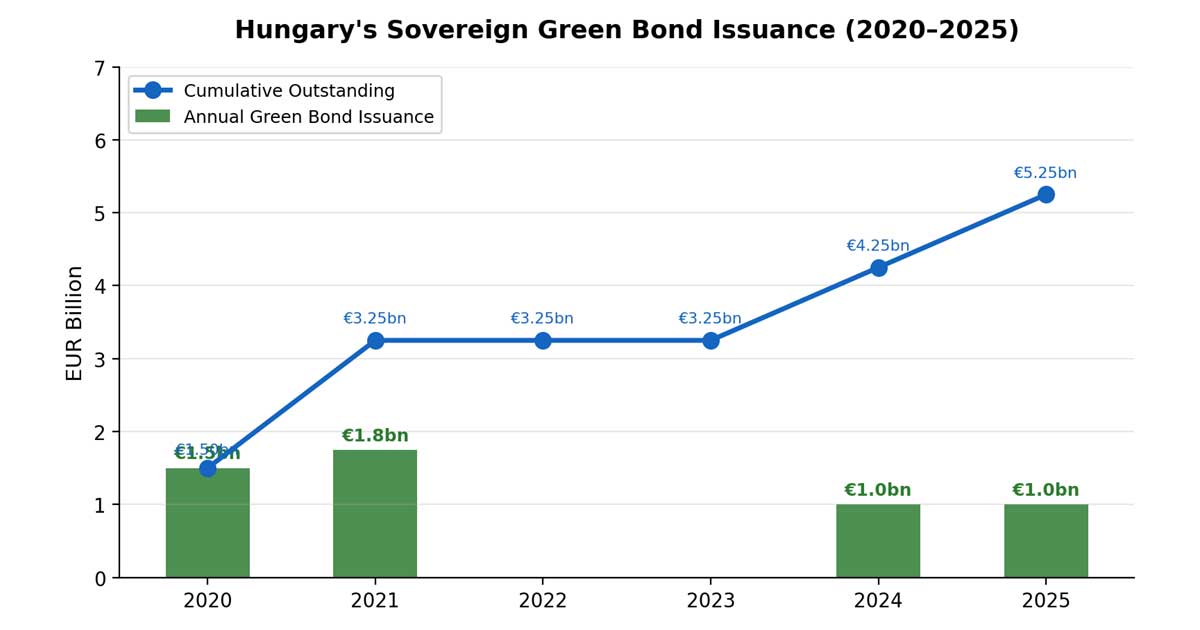

The ÁKK’s Sovereign Green Bond Programme: International Recognition

Hungary’s sovereign green bond programme, managed by the ÁKK, has emerged as one of the most internationally acclaimed green debt initiatives in Central and Eastern Europe. Hungary issued its inaugural green bond in June 2020, raising €1.5 billion with a 15-year maturity and a fixed coupon of 1.75 percent. Investor demand was exceptional, with oversubscription exceeding fivefold, and the bond was sold at a spread 50 basis points tighter than the original price guidance. Since then, Hungary has issued additional green bonds in multiple currencies, including euro, Japanese yen, and renminbi tranches, reflecting a deliberate strategy of maximum funding diversification.

Figure 3. Hungary’s sovereign green bond issuance and cumulative outstanding volume (2020–2025). Source: Compiled from ÁKK publications and ING Research (2024, 2025).

Figure 3. Hungary’s sovereign green bond issuance and cumulative outstanding volume (2020–2025). Source: Compiled from ÁKK publications and ING Research (2024, 2025).

In January 2025, the ÁKK entered international bond markets with a €2.5 billion dual-tranche issuance comprising a €1.5 billion conventional 10-year bond and a €1 billion 15-year green bond. The green tranche was approximately four times oversubscribed, demonstrating sustained international investor appetite for Hungarian green sovereign debt. This transaction earned the ÁKK two prestigious awards from Global Capital: Most Notable Issuer of the Year in Central and Eastern Europe and Most Notable ESG Issuer of the Year in the CEEMEA region. Previously, in 2024, the ÁKK received the Impact Report of the Year award from Environmental Finance for the quality and transparency of its integrated green bond allocation and impact reporting.

Green bond proceeds are allocated to central government expenditures across eight eligible categories: clean transportation, renewable energy, energy efficiency, land use and living natural resources, pollution prevention and control, sustainable water and wastewater management, climate change adaptation, and research and innovation. The ÁKK’s updated Green Bond Framework, released in 2023, aligns with evolving market standards and investor expectations, reinforcing Hungary’s commitment to transparent and impactful green finance.

Renewable Energy Expansion as an ESG Foundation

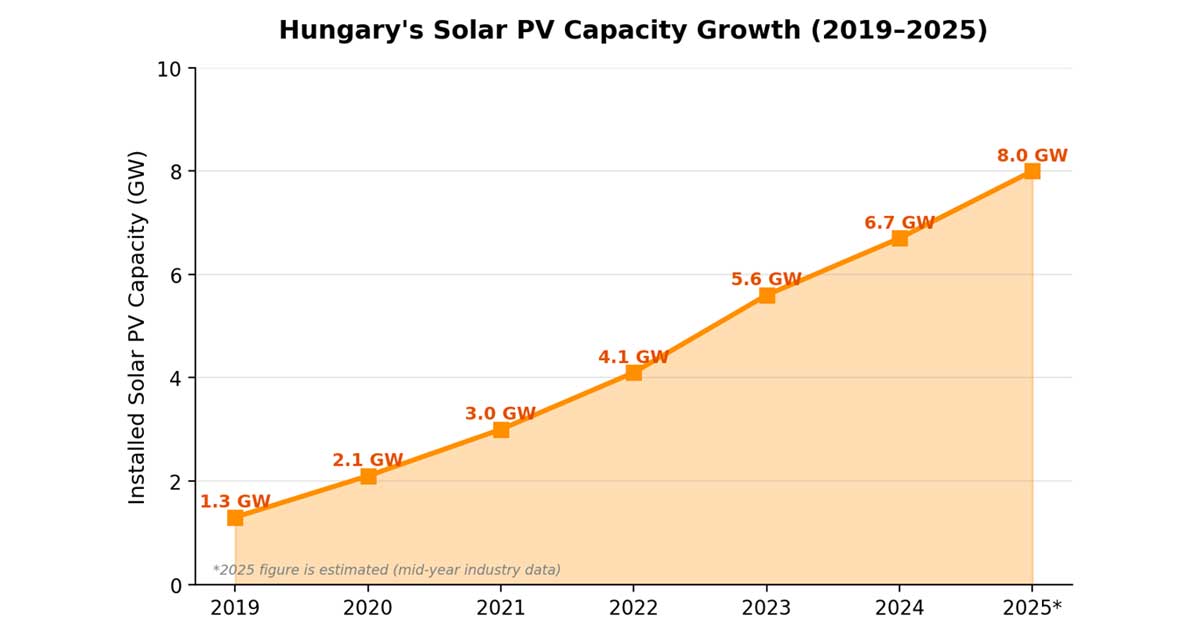

Hungary’s green finance ecosystem is reinforced by rapid progress in renewable energy deployment. Solar photovoltaic capacity has grown remarkably, surpassing 6.7 GW by mid-2024 and approaching an estimated 8 GW by mid-2025, far exceeding earlier trajectory projections. Hungary’s updated National Energy and Climate Plan set a target of at least 30 percent renewable energy in gross final consumption by 2030, up from approximately 17 percent in 2023. The liberalization of wind energy regulations from 1 January 2024, including the reduction of setback distances from 12 kilometers to 700 meters, has further opened new development pathways.

Figure 4. Growth of installed solar PV capacity in Hungary (2019–2025). Source: MAVIR data as cited by Chambers and Partners (2025) and industry reporting.

Figure 4. Growth of installed solar PV capacity in Hungary (2019–2025). Source: MAVIR data as cited by Chambers and Partners (2025) and industry reporting.

This renewable energy expansion creates a mutually reinforcing dynamic with the country’s green finance infrastructure. The proceeds from sovereign green bonds directly finance clean energy and transport projects, while the growing renewable capacity strengthens Hungary’s ESG profile and reduces transition risk in banking portfolios. The interplay between green bond issuance, MNB supervisory incentives, and renewable energy investment thus creates an integrated ecosystem that enhances both financial stability and environmental sustainability.

Political and Economic Tensions

Across Europe, mounting resistance to regulatory overload has already led to selective rollbacks and implementation delays. This political reality underscores the need for pragmatic governance. Excessive regulatory rigidity risks undermining economic growth, fuelling Euroscepticism, and weakening public support for sustainability policies.

Hungary’s position reflects this broader European debate. The government has consistently emphasized the primacy of economic competitiveness, energy security, and industrial development. Within this framework, ESG compliance must be integrated into a broader strategy of national economic resilience rather than imposed as an externally driven regulatory burden.

The December 2025 Omnibus agreement validates many of Hungary’s longstanding arguments regarding proportionality and competitive burden. The significant narrowing of CSRD scope and the delay in implementation timelines reflect a broader European recognition that sustainability regulation must be calibrated to economic reality. Hungary’s consistent advocacy for SME protection and administrative simplification has contributed to shaping this outcome, demonstrating that assertive engagement in EU negotiations can yield tangible results for national interests.

Conclusion

The EU’s greenwashing crackdown marks a profound transformation of sustainability governance. By embedding ESG transparency into corporate law, consumer protection, and financial supervision, Brussels seeks to restore credibility and accelerate the green transition. Yet the scale and complexity of the regulatory framework raise legitimate concerns regarding administrative burden, economic competitiveness, and regulatory proportionality. The Omnibus simplification, while welcome, does not eliminate these tensions but rather recalibrates their intensity.

For Hungary, the challenge lies in navigating this transformation in a way that preserves economic dynamism, protects national interests, and enhances long-term development prospects. Strategic adaptation, regulatory pragmatism, and targeted support for domestic enterprises will be essential to turning regulatory obligation into economic opportunity.

Critically, Hungary’s proactive investments in green finance infrastructure through the MNB’s Green Program, the ÁKK’s internationally recognized sovereign green bond programme, and the rapid expansion of renewable energy capacity provide a strong foundation for this transition. These achievements demonstrate that Hungary is not merely responding to EU regulatory pressure but actively shaping its sustainable finance landscape in ways that enhance investor confidence, strengthen financial system resilience, and support long-term economic modernization.

Rather than viewing the EU’s ESG agenda as a constraint, Hungary can leverage the transition to promote industrial modernization, energy efficiency, and technological innovation. In doing so, it can safeguard national competitiveness while contributing constructively to Europe’s broader sustainability ambitions.

References

Chambers and Partners. (2025). Renewable energy 2025: Hungary. In Global practice guides. Chambers and Partners. https://practiceguides.chambers.com/practice-guides/renewable-energy-2025/hungary

Environmental Finance. (2024). Impact report of the year (for issuers): Government Debt Management Agency (ÁKK). Environmental Finance Sustainable Debt Awards 2024. https://www.environmental-finance.com/content/awards/environmental-finances-sustainable-debt-awards-2024/

European Commission. (2020). A new circular economy action plan: For a cleaner and more competitive Europe. European Commission.

European Commission. (2021). Proposal for a directive empowering consumers for the green transition. European Commission.

European Commission. (2025a). Omnibus simplification package: Sustainability. Directorate-General for Financial Stability, Financial Services and Capital Markets Union. https://finance.ec.europa.eu/news/omnibus-package-2025-04-01_en

European Commission. (2025b). Simplification: Omnibus proposals. European Commission. https://commission.europa.eu/law/law-making-process/better-regulation/simplification-and-implementation/simplification_en

European Financial Reporting Advisory Group (EFRAG). (2023). European Sustainability Reporting Standards (ESRS). EFRAG.

European Parliament. (2025). Hungary’s climate action strategy (Briefing PE 769.532). European Parliamentary Research Service. https://www.europarl.europa.eu/RegData/etudes/BRIE/2025/769532/

European Parliament & Council of the European Union. (2022). Directive (EU) 2022/2464 on corporate sustainability reporting (CSRD). Official Journal of the European Union.

European Parliament & Council of the European Union. (2025). Directive (EU) 2025/794 (Stop-the-Clock). Official Journal of the European Union.

GKI Gazdaságkutató Zrt. (2025, April 29). Has competitiveness taken priority over sustainability in the EU? Implications for Hungarian companies. GKI. https://gki.hu/language/en/2025/04/29/has-competitiveness-taken-priority-over-sustainability-in-the-eu-implications-for-hungarian-companies/

Green Central Banking. (2024, January 16). ‘We intend to be proactive, leading by example’: Why Hungary is racing ahead on green finance. Green Central Banking. https://greencentralbanking.com/2024/01/16/hungary-green-monetary-policy-scorecard-mnb/

Hungary Today. (2025, June 20). Hungary named best bond issuer in the region by Global Capital. Hungary Today. https://hungarytoday.hu/hungary-named-best-bond-issuer-in-the-region-by-global-capital/

ING. (2025, January 23). Hungary: Reorientation back to HGBs issuance. ING Think. https://think.ing.com/articles/hungary-reorientation-back-to-hgbs-issuance/

Kim, D., Raciborski, E., & Várgedő, B. (2024). Experiences from the MNB’s Green Preferential Capital Requirement Programme and the extension of the Programme. Financial and Economic Review, 23(3), 193–209. https://hitelintezetiszemle.mnb.hu/en/fer-23-3-fa1-kim-raciborski-vargedo

KnowESG. (2023, July 26). Hungary updates Green Bond Framework. KnowESG. https://www.knowesg.com/sustainable-finance/hungary-updates-green-bond-framework-26072023

Magyar Nemzeti Bank. (2024a). Green Finance Report, July 2024. Magyar Nemzeti Bank. https://www.mnb.hu/en/publications/reports/green-finance-report

Magyar Nemzeti Bank. (2024b). Green finance and sustainability were the main focus at the Magyar Nemzeti Bank’s Technical Cooperation Programme for partner central banks [Press release]. https://www.mnb.hu/en/pressroom/press-releases/press-releases-2024/

Magyar Nemzeti Bank. (2025). Recommendation No. 7/2025 (VI. 23.) on the application of a minimum ESG questionnaire in credit risk assessment. Magyar Nemzeti Bank. https://zoldpenzugyek.mnb.hu/

OECD. (2022). Environmental policy and corporate competitiveness. OECD Publishing.

Polgári Szemle. (2020). Certain issues of green bonds and their perception by financial markets, with focus on Hungary. Polgári Szemle, 16(Special Issue). eng.polgariszemle.hu/images/content/pdf/psz_2020_16_eng_27.pdf

PwC. (2023). CSRD and ESG reporting: Transforming corporate governance in Europe. PricewaterhouseCoopers. https://www.pwc.com

PwC. (2025, December). EU reaches compromise on ‘Omnibus’ proposals. PwC Viewpoint. https://viewpoint.pwc.com/gx/en/pwc/in-briefs/ib_int202527.html

Reuters. (2026). EU countries approve revised sustainability reporting rules amid competitiveness concerns. Reuters. https://www.reuters.com