In December 2025, news emerged that the European Union might abandon its plan to ban the registration of passenger cars and light commercial vehicles equipped with conventional internal combustion engines (ICE) in Member States from 2035 onwards. Under the revised approach, the objective would no longer be a full ban, but rather a 90% reduction in tailpipe emissions—meaning that the EU would effectively step back from the idea of a complete prohibition.

About the regulation and the proposed amendment

On 16 December 2025, it became public that the EU may partially withdraw from its plan to ban the registration of passenger cars and light commercial vehicles fitted with conventional engines from 2035. Until now, the EU has insisted—almost rigidly—on a climate-policy requirement according to which, from 2035 onwards, only vehicles with zero CO₂ emissions could be sold in these two categories. The goal was to cut carbon dioxide emissions in this segment by 100% compared to 2021 levels.

The European Commission is now proposing to amend this concept, although the Council and the European Parliament must also approve the change. The revised programme focuses on a 90% reduction in tailpipe emissions, which signals a retreat from the full ban. However, the twist is that the Commission ultimately expects manufacturers to compensate for the remaining 10% gap through other measures—for example, by purchasing steel products with a lower carbon footprint.[1] In this sense, the concession can hardly be considered a major sectoral relief.

Since the EU’s ideas first emerged, I have consistently spoken out against a full ban. In this analysis—drawing on multiple perspectives and arguments—I aim once again to shed light on why this change became necessary and why, in my view, the rules should be softened even further.

The ban on internal combustion engines from a climate policy perspective

Overall, the EU regulation has not achieved the desired outcomes from an environmental perspective—let us examine why.

According to EU data, nearly one fifth of greenhouse gas emissions are linked to road transport, particularly passenger cars and light commercial vehicles. For this reason, manufacturers have had to comply with unified fleet-level CO₂ targets since 2021. At first glance, EU intervention in this area therefore seems understandable.[2]

Yet despite the very strict regulatory environment, emissions from transport and road transport remain higher than they were when the regulation entered into force, and have not decreased meaningfully in recent years.[3]

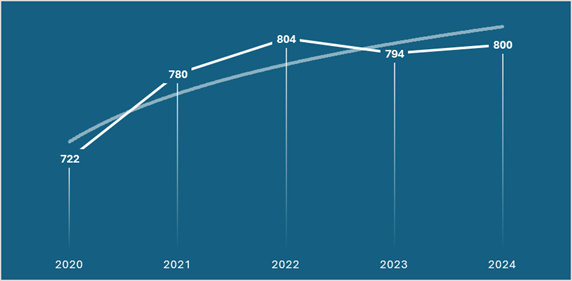

Figure 1. Carbon dioxide emissions in the transport sector (million tonnes CO₂ equivalent GHG; source: EEA)

Between 2020 and 2024, greenhouse gas emissions in the EU transport sector increased by approximately 11%.[4] One could argue that without strict rules emissions would have grown even more—but this is not necessarily true. Based on the different methodologies, time series publications and estimates of major international organisations, one may conclude that between 2020 and 2024 global transport emissions did not significantly differ from those in the EU, despite the fact that similarly strict rules were not implemented worldwide.[5] While the EU introduced numerous far-reaching requirements, the atmospheric concentration of greenhouse gases continued to rise globally in the same period. Between 2020 and 2024, CO₂ concentration increased from 413.2 ppm to 423.9 ppm.[6]

The ban on internal combustion engines from an economic and social perspective

EU regulation has produced unhealthy economic conditions in car manufacturing and has caused severe damage to the industry.

Europe has well-known traditions and achievements in automotive manufacturing, yet there is no certainty this will remain true in the future. In global competition, the EU has already lost ground to Asian and American challengers in areas such as IT, digitalisation, space technology, artificial intelligence and semiconductor manufacturing. The automotive industry may be seen as one of the EU’s last major key sectors—yet today it is rapidly losing competitiveness.

The Draghi Report also addresses this point by stating that bureaucracy and poorly designed environmental regulations harm the performance of key EU industries.[7]

The lack of foresight among EU decision-makers has resulted in sectoral anomalies. A striking example is that in October 2024—allegedly to protect the European automotive industry—the EU imposed countervailing tariffs on Chinese electric vehicle imports of up to 45%, affecting models such as Tesla manufactured in China and imported into the EU, as well as BYD vehicles. At the same time, for climate policy reasons, the EU obliged European manufacturers to pay penalties or purchase CO₂ credits from other automotive firms if they could not meet centrally set CO₂ reduction quotas (CO₂ pooling).

As a result, an unusual contradiction emerged: while the EU imposed tariffs supposedly to protect its industry from companies such as Tesla or BYD, it simultaneously forced its own manufacturers to transfer large sums of money to the very same competitors by purchasing CO₂ credits from them. Moreover, the combined effect of tariffs and CO₂ requirements was that consumers had to buy vehicles at ever higher prices in European dealerships.

In some cases, the factory performance of certain car models was artificially reduced in order to meet EU emission requirements—meaning customers suffered on multiple fronts, since in Asian or American markets the same vehicle could have been purchased at a lower price and with higher engine performance than in the EU.

Due to declining investment, shrinking R&D expenditure, excessive bureaucracy, high labour and energy costs, and an ill-considered green transition, European automotive manufacturing has gone into decline. Over the past two years, announced or implemented layoffs by automotive manufacturers and suppliers in Europe have affected nearly 100,000 employees.

Figure 2. Major announced or implemented layoffs in the EU automotive industry since 2024 (source: author’s collection)

A portion of the layoffs resulted from the fact that—contrary to manufacturers’ expectations—EU citizens purchased fewer fully electric cars. This was mainly due to high prices, shortcomings in charging infrastructure, rising charging costs, and insufficient driving range.

The situation is further complicated by the fact that while the EU imposes protective tariffs on Chinese industry and trade, EU electric vehicle manufacturing is heavily dependent on Chinese producers. While Fit for 55—abandoning the principle of technological neutrality—made it practically conceivable only to allow fully electric cars to be placed on the EU market from 2035, the EU ignored the fact that it controls only around 7% of the battery industry required for EV production, while the market for raw material production needed for batteries is dominated 87% by the US and China.[8]

In theory, the EU does not favour only fully electric cars. A zero-emission level could also be achieved through other technologies—such as hydrogen propulsion. In practice, however, these alternative technologies remain far from mass deployment in market and technical terms. The failure to recognise these problems once again reveals a complete lack of policy foresight.

The weaknesses of the European automotive industry have become a major challenge, since the sector accounts for 7% of EU GDP, and including related companies and supply chains it provides livelihoods for 13.8 million people.[9] The EU automotive market has begun to shrink significantly in several dimensions.

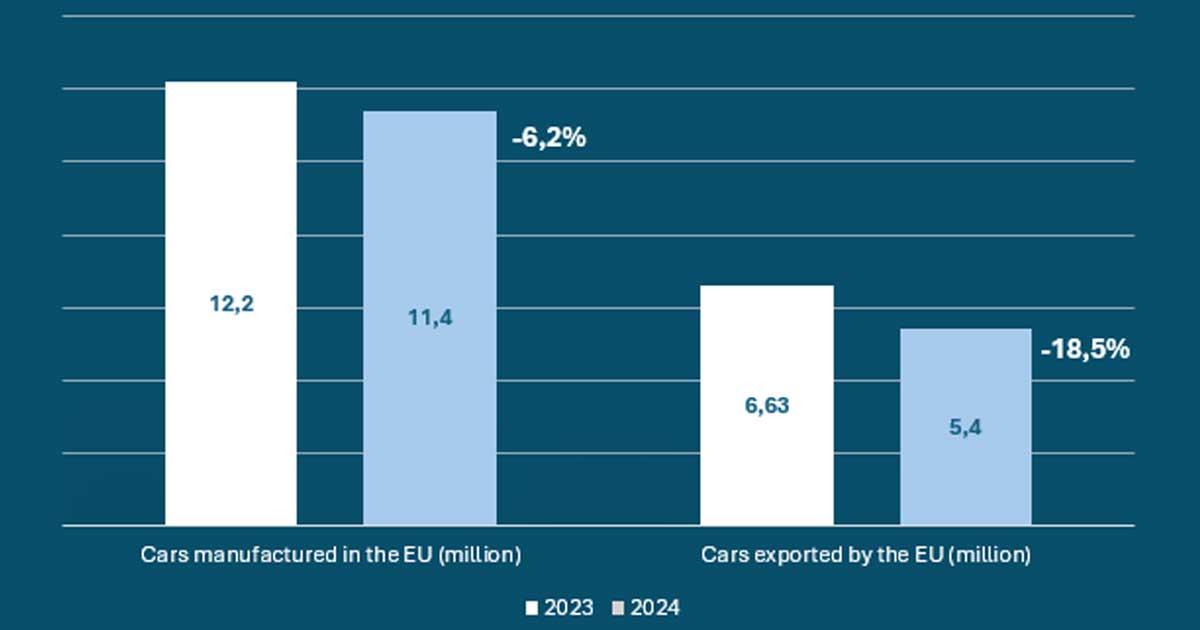

Figure 3. Developments in EU car production and export volume, 2023–2024 (source: ACEA) [10]

Figure 3. Developments in EU car production and export volume, 2023–2024 (source: ACEA) [10]

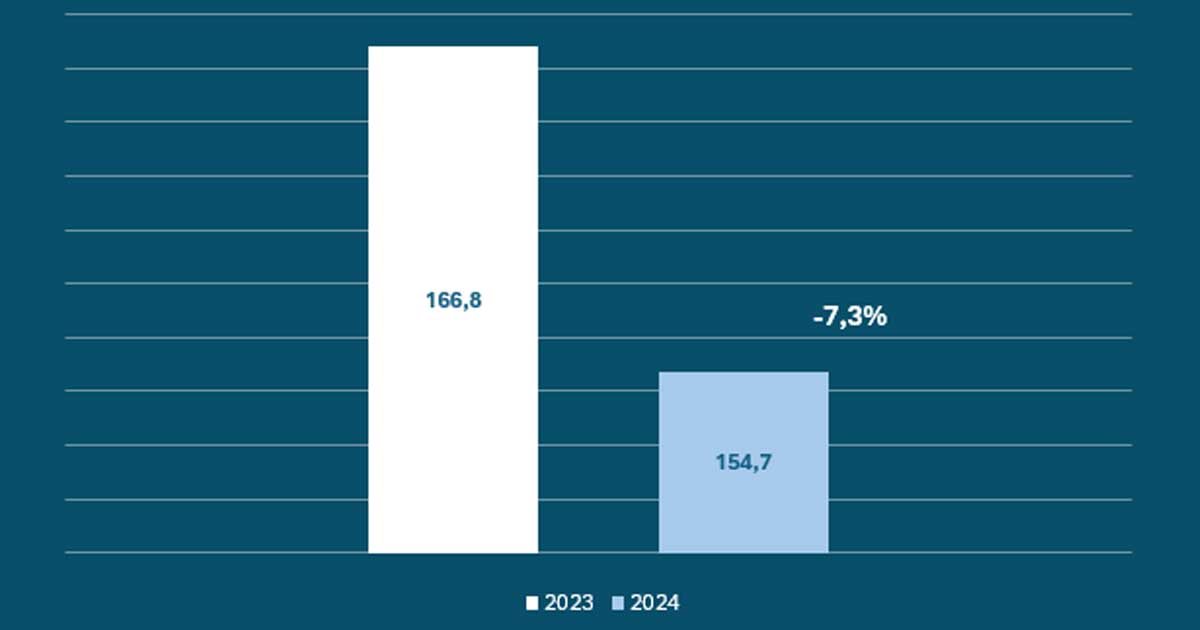

Figure 4. Change in EU automotive export volume, 2023–2024 (source: ACEA) [11]

Figure 4. Change in EU automotive export volume, 2023–2024 (source: ACEA) [11]

The number of cars produced in Europe has fallen, as have exports and the revenues generated from them. Profitability has decreased mainly due to the success of Asian brands. Alongside Japanese and South Korean models, Chinese car types—only a few years ago considered laughable—have risen explosively. A telling figure: the share of cars manufactured in China or imported from there among fully electric vehicles sold in the EU was only 4.9% in 2020, yet grew to 29.3% by 2023.[12]

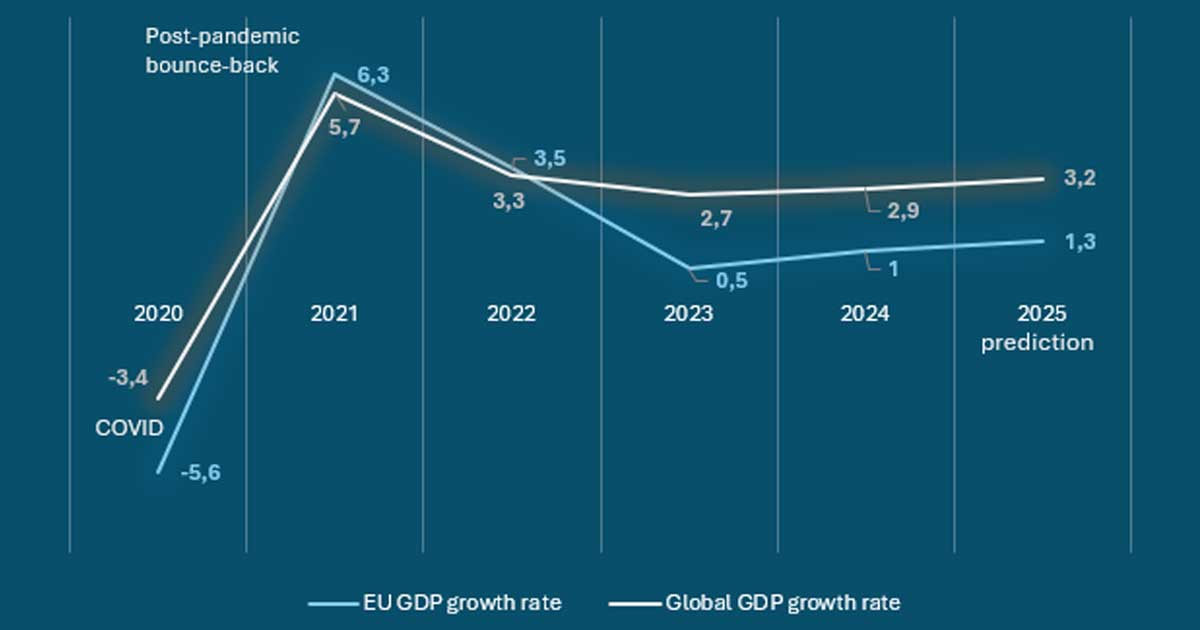

The struggling automotive industry has also contributed to the fact that from 2023 onwards the EU’s GDP growth rate has diverged significantly from the global trend.[13] Over the past three years, growth in gross domestic output has been less than one third of the global average. Since EU growth is part of global growth, the gap between EU GDP growth and that of non-EU economies is even wider than this comparison suggests.

Figure 5. GDP growth rates in the EU and globally, % (sources: European Commission, Eurostat, OECD)

Figure 5. GDP growth rates in the EU and globally, % (sources: European Commission, Eurostat, OECD)

In addition to mass job losses, Fit for 55 has another societal dimension that is rarely discussed, even though its negative market-shock effects could be substantial. As early as 2022, I wrote that in my view the full ban on internal combustion engines scheduled for 2035 would be socially unfair and economically irrational.[14] There are around 260 million passenger cars in circulation in the EU, at least 90% of which are not fully electric (diesel, petrol, hybrid). This means that conventional cars represent a very significant form of private wealth across the EU. As the 2035 deadline approached, citizens would have been forced to accept an asymmetrical, large-scale loss in value of this wealth.

Based on the economic logic of so-called stranded assets, the used-car market would have begun to heavily discount non-electric vehicles. Many car owners from the lowest social strata would not have been able to switch to fully electric cars even with targeted state subsidies—thereby increasing social disparities and tensions, which directly contradicts EU principles.

The December 2025 intention to amend the full ban by reducing the quota to 90% does not automatically solve the problem, yet it has helped to mitigate the approaching market and social shock.

Conclusions

The EU regulation aiming at the complete ban on passenger cars and light commercial vehicles with conventional powertrains, and the preferential treatment of fully electric vehicles in this category, has proven to be a serious strategic mistake. Numerous data points demonstrate that the EU has suffered substantial damage in terms of social and economic competitiveness, while Europe’s geopolitical position has deteriorated and climate objectives have not been fully achieved.

After years of delay, the softening of the regulation is finally pointing in the right direction. However, in my view, the extent of relief is still insufficient. It would be essential to harmonise business, social and environmental interests in the automotive industry—and to respect the principle of technological neutrality, encouraging competition between different technologies.

Hungary provides a good example in this regard. The Budapest Declaration, adopted at the end of Hungary’s EU Presidency, was drafted precisely in the spirit of aligning economic, social and environmental interests.[15] The European Union should take its content seriously and finally implement its twelve points.

Hungary believes in connectivity and technological neutrality. The country has supported the settlement of both Asian and European automotive manufacturers and suppliers alike, and simultaneously encourages the use of conventional, hybrid and battery-based technologies. A similarly prudent approach would be needed within the institutional system of the European Union.

[1] European Commission (2025). Automotive Package. Brussels: European Commission. Source: https://transport.ec.europa.eu/transport-themes/clean-transport-urban-transport/road-transport-reducing-co2-emissions-vehicles/boosting-european-car-sector/automotive-package_en (accessed: 17 December 2025).

[2] European Commission (2025). Cars and Vans – Climate Action. Brussels: European Commission. Source: https://climate.ec.europa.eu/eu-action/transport-emissions/road-transport/cars-and-vans_en (accessed: 18 December 2025).

[3] European Environment Agency (2025). Greenhouse gas emissions from transport in Europe. Copenhagen: EEA. Source: https://www.eea.europa.eu/en/analysis/indicators/greenhouse-gas-emissions-from-transport (accessed: 18 December 2025).

[4] It should be noted that 2020 was an exceptional year due to COVID-19; therefore, the increase between 2020 and 2024 can partly be interpreted as a rebound effect.

[5] International Energy Agency (2023). Tracking Transport. Paris: IEA. Source: https://www.iea.org/energy-system/transport (accessed: 19 December 2025).

World Bank (2024). Carbon dioxide (CO2) emissions from Transport. Washington, DC: World Bank. Source: https://data.worldbank.org/indicator/EN.GHG.CO2.TR.MT.CE.AR5 (accessed: 20 December 2025).

United Nations Environment Programme (UNEP) (2025). Emissions Gap Report 2024. Nairobi: UNEP. Source: https://www.unep.org/interactives/emissions-gap-report/2024/emissions-gap-report/2024 (accessed: 19 December 2025).

[6] World Meteorological Organization (2025). WMO Greenhouse Gas Bulletin – No. 21. Geneva: WMO. Source: https://public.wmo.int/publication-series/wmo-greenhouse-gas-bulletin-no-21 (accessed: 20 December 2025).

World Meteorological Organization (2021). WMO Greenhouse Gas Bulletin – No. 17. Geneva: WMO. Source: https://library.wmo.int/records/item/58705-no-17-25-october-2021#.ZBMRW-zMJgE (accessed: 20 December 2025).

[7] Draghi, Mario (2024). The Future of European Competitiveness: Report to the European Commission. Brussels. Source: https://commission.europa.eu/topics/competitiveness/draghi-report_en#paragraph_47059 (accessed: 19 December 2025).

[8] European Automobile Manufacturers’ Association (ACEA) (2024). EU Battery Supply Chain & Import Reliance. Brussels: ACEA. Source: https://www.acea.auto/files/ACEA_Fact_sheet-EU_battery_supply_chain_and_import_reliance_.pdf (accessed: 2 January 2026).

[9] European Commission (2025). Boosting the European car sector. Brussels: European Commission. Source: https://commission.europa.eu/topics/business-and-industry/boosting-european-car-sector_en (accessed: 19 December 2025).

European Parliament (2024). The crisis facing the EU’s automotive industry. Brussels: EPRS. Source: https://www.europarl.europa.eu/RegData/etudes/ATAG/2024/762419/EPRS_ATA%282024%29762419_EN.pdf (accessed: 16 December 2025).

[10] European Automobile Manufacturers’ Association (ACEA) (2024). EU vehicle trade, by vehicle type (in units). Brussels: ACEA. Source: https://www.acea.auto/figure/eu-motor-vehicle-trade-by-vehicle-type-in-units/ (accessed: 21 December 2025).

European Automobile Manufacturers’ Association (ACEA) (2025). The Automobile Industry Pocket Guide 2025/2026. Brussels: ACEA. Source: https://www.acea.auto/publication/the-automobile-industry-pocket-guide-2025-2026/ (accessed: 15 December 2025).

[11] European Automobile Manufacturers’ Association (ACEA) (2025). Economic and Market Report: Global and EU auto industry – Full year 2024. Brussels: ACEA. Source: https://www.acea.auto/files/Economic_and_Market_Report-Full_year-2024.pdf (accessed: 21 December 2025).

[12] European Parliament (2024). The crisis facing the EU’s automotive industry. Figure 2. Brussels: EPRS. Source: https://www.europarl.europa.eu/RegData/etudes/ATAG/2024/762419/EPRS_ATA%282024%29762419_EN.pdf (accessed: 16 December 2025).

[13] Naturally, significant factors also played an important role here, such as the Russia–Ukraine war and its consequences (e.g. sanctions and high energy prices).

[14] Kitta, Gergely (2022). Burying or Surviving: The Fate of Internal Combustion Engines in the EU. Index.hu. 18 July 2022. Source: https://index.hu/velemeny/2022/07/18/temetni-vagy-tulelni-a-belso-egesu-motorok-sorsa-az-eu-ban/ (accessed: 21 December 2025)

[15] European Council (2024). Budapest Declaration on the New European Competitiveness Deal. Brussels: European Council. Source: https://www.consilium.europa.eu/hu/press/press-releases/2024/11/08/the-budapest-declaration/ (accessed: 3 January 2026).