The growing prominence of nature-positive finance within the European Union reflects a broader transformation in how financial markets perceive environmental constraints and opportunities, particularly regarding biodiversity. While climate change has long dominated sustainability discourse, biodiversity loss is increasingly recognized as an equally systemic risk to economic stability and long-term prosperity. The European Union, through its regulatory frameworks and strategic policy initiatives, has begun to embed biodiversity considerations into financial decision-making processes, thereby accelerating the integration of biodiversity metrics into mainstream investing. Within this context, Hungary, as a committed member state, has both the opportunity and responsibility to align national financial practices with these emerging European priorities, while maintaining a pragmatic and sovereignty-conscious approach that supports national economic interests.

Strengths and weaknesses of past conservation policies and practice in the European Union, as well as opportunities and challenges for conservation in the coming decade.

Source: Milieu, L., ICFI (2015).

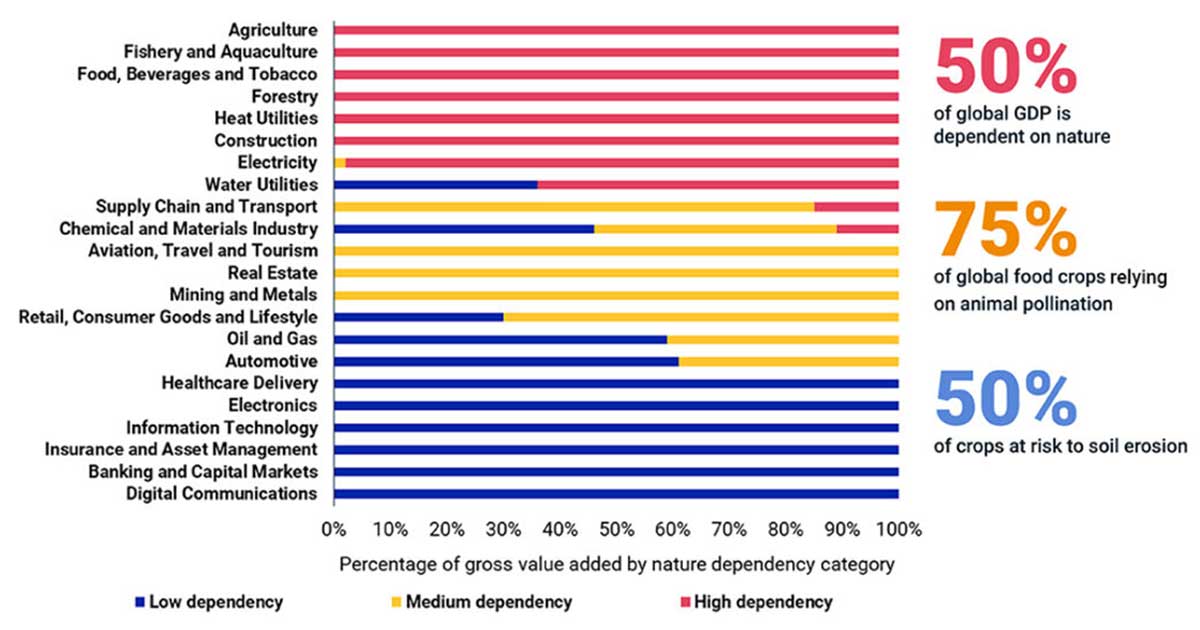

The concept of nature-positive finance refers to financial flows that actively contribute to halting and reversing biodiversity loss, rather than merely minimizing environmental harm. This represents a shift from traditional environmental risk management toward a more proactive investment paradigm, where capital allocation is used as a lever to generate measurable ecological benefits. As recent research highlights, economic activity is deeply intertwined with natural systems, with a significant share of global GDP dependent on ecosystem services, yet biodiversity continues to decline at an alarming rate due to human pressures. Consequently, financial markets are increasingly expected to account for biodiversity impacts in a systematic and quantifiable manner.

Global Dependencies of Industries on Natural Capital, MSCI

Source: Gustavsson, A. (2023).

Source: Gustavsson, A. (2023).

Nature-Positive Finance and the Evolution of Biodiversity Metrics

The emergence of biodiversity metrics in finance has been driven by the recognition that existing sustainability tools, largely focused on carbon emissions, are insufficient to capture the complexity of ecological degradation. Unlike greenhouse gas emissions, biodiversity lacks a single, universally accepted unit of measurement, which complicates efforts to standardize reporting and investment assessment. Nevertheless, recent developments in impact measurement frameworks, including life cycle assessment approaches and biodiversity foot printing methods, have begun to address this gap by providing structured ways to evaluate environmental pressures and outcomes.

Life cycle assessment LCA framework

Sources: Golsteijn, L. (2022).

Sources: Golsteijn, L. (2022).

Two principal approaches have emerged in the measurement of biodiversity impacts: state-based metrics and pressure-based metrics. State-based metrics focus on the actual condition of ecosystems and species, while pressure-based metrics assess the drivers of biodiversity loss, such as land use change, pollution, and resource extraction. The latter approach is particularly relevant for financial institutions, as it allows for the estimation of potential impacts based on economic activities and investment portfolios. This distinction is crucial in the context of nature-positive finance, where investors must evaluate not only current impacts but also future trajectories.

Importantly, the integration of biodiversity metrics into investment decisions represents a transition from qualitative sustainability narratives to quantitative, data-driven analysis. As noted in the literature, many corporate disclosures remain largely descriptive, with limited use of standardized indicators or outcome-based measurements. The EU’s regulatory push seeks to correct this imbalance by mandating more rigorous and comparable reporting practices, thereby enhancing transparency and accountability in financial markets.

European Union Policy Framework and Strategic Direction

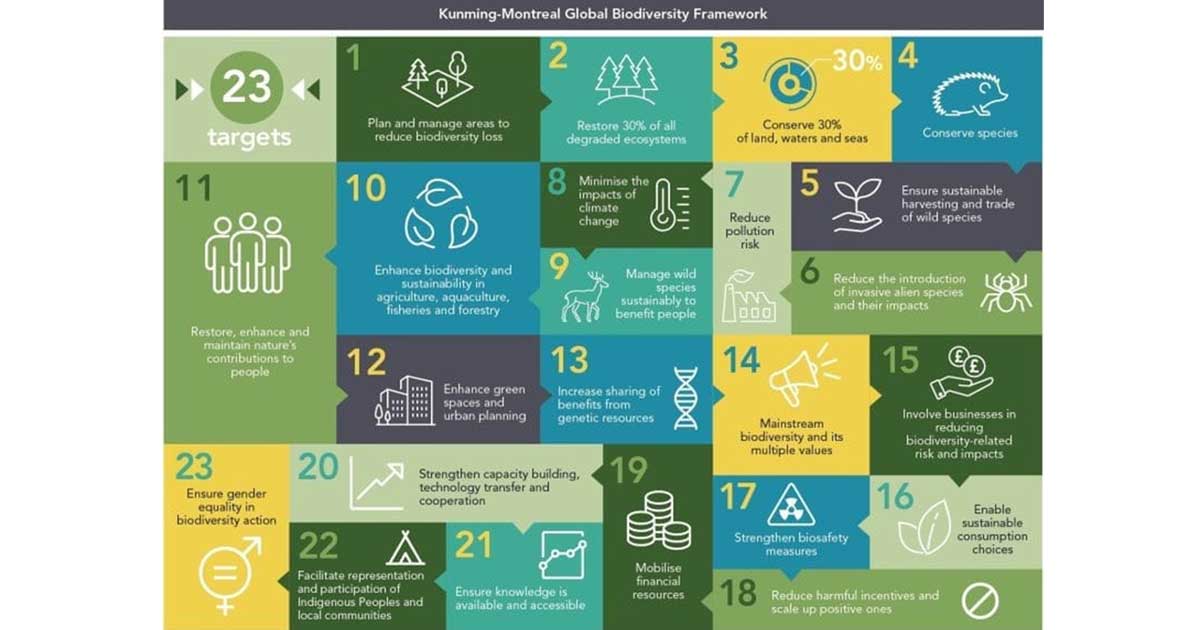

The European Union has taken a leading role in advancing nature-positive finance through a comprehensive set of policy instruments, most notably the EU Biodiversity Strategy for 2030 and the Sustainable Finance framework. These initiatives are closely aligned with the global Kunming-Montreal Global Biodiversity Framework, which emphasizes the need for private sector engagement in biodiversity conservation and restoration.

Kunming Montreal biodiversity framework targets

Source: Nature Positive. (2026).

A central element of the EU approach is the requirement for financial institutions and large corporations to assess, disclose, and manage their biodiversity-related risks and impacts. This is reflected in the Corporate Sustainability Reporting Directive (CSRD) and the development of the European Sustainability Reporting Standards (ESRS), which include specific provisions for biodiversity and ecosystems. By embedding biodiversity considerations into financial disclosures, the EU aims to redirect capital flows toward sustainable activities and reduce investments in nature-negative sectors.

Furthermore, the EU Taxonomy Regulation plays a critical role in defining what constitutes environmentally sustainable economic activity. Although initially focused on climate objectives, the taxonomy has progressively expanded to encompass all six environmental objectives, including the protection and restoration of biodiversity and ecosystems. The Environmental Delegated Act, formally published in November 2023 and applicable from January 2024, introduced Technical Screening Criteria for economic activities making a substantial contribution to non-climate environmental objectives, including biodiversity protection and restoration, sustainable use and protection of water and marine resources, transition to a circular economy, and pollution prevention and control. This regulatory expansion provides investors with a significantly more comprehensive framework for identifying nature-positive investments across a broader range of economic activities.

The EU Taxonomy in 2026: Simplification, Expansion, and Biodiversity Alignment

The year 2026 represents a pivotal moment in the evolution of the EU Taxonomy and its relevance to nature-positive finance. As of the 2026 reporting cycle, alignment reporting under the Taxonomy has been extended to cover all six environmental objectives, including biodiversity and ecosystems, water and marine resources, circular economy, and pollution prevention, in addition to the climate objectives already in force. This means that for the first time, financial institutions and large corporations subject to the Corporate Sustainability Reporting Directive (CSRD) are required to report not merely on the eligibility of their activities under these objectives, but on their actual alignment with the corresponding Technical Screening Criteria. The practical significance of this shift for nature-positive finance cannot be overstated, as it transforms biodiversity from an aspirational reporting category into a binding disclosure obligation with measurable performance indicators.

At the same time, the European Commission has introduced notable simplification measures through Delegated Regulation (EU) 2026/73, which took effect at the beginning of 2026. These measures include streamlined reporting templates with fewer data points, a 10 per cent materiality threshold that exempts non-material economic activities from full taxonomy alignment assessment, and simplified “Do No Significant Harm” (DNSH) criteria for certain objectives such as pollution prevention and control. For non-financial companies, activities accounting for less than 10 per cent of revenue, capital expenditure, or operating expenses may be exempted from detailed eligibility and alignment assessment. Furthermore, the updated regulation provides the option for companies to waive the operating expenditure taxonomy audit if such expenditures are not material to their business model. These simplifications are part of a broader effort under the Commission’s Omnibus I package to reduce administrative burdens while maintaining the integrity of sustainability objectives.

Additionally, the scope of the Taxonomy has expanded significantly in terms of the entities covered. From the 2026 financial year, all large companies falling within the scope of the CSRD are required to report on their taxonomy alignment, with capital market-oriented small and medium-sized enterprises (SMEs) expected to follow from 2027. For financial institutions, the green asset ratio, which reflects the proportion of taxonomy-aligned lending and investment portfolios, has also been subject to updated disclosure requirements as specified by the European Banking Authority. This progressive widening of the reporting base is expected to generate a substantially richer dataset on the biodiversity-related performance of economic activities across the European economy, thereby enhancing the ability of investors and regulators to assess the nature-positive credentials of financial portfolios.

Critically, the EU Taxonomy’s approach to biodiversity remains anchored in the principle that an activity must make a substantial contribution to at least one environmental objective while doing no significant harm to the others, and must comply with minimum social safeguards. For activities contributing to the biodiversity objective specifically, the Technical Screening Criteria require demonstrable contributions to preserving habitats, promoting ecosystem restoration, and preventing ecosystem degradation. This science-based, criteria-driven approach is essential for establishing market credibility and preventing greenwashing in nature-positive finance. Early evidence suggests that companies reporting alignment with the Taxonomy exhibit improved market valuations and profitability, reinforcing the business case for biodiversity integration.

Mainstreaming Biodiversity in Investment Practices

The incorporation of biodiversity metrics into mainstream investing reflects a broader transformation in financial markets, where environmental considerations are increasingly viewed as material to financial performance. Investors are recognizing that biodiversity loss can generate significant risks, including supply chain disruptions, regulatory penalties, and reputational damage. At the same time, nature-positive investments offer substantial opportunities, particularly in sectors such as sustainable agriculture, forestry, and ecosystem restoration.

Impact investing has emerged as a key mechanism for channelling capital into nature-positive activities. Unlike traditional investment strategies, impact investing seeks to generate measurable environmental outcomes alongside financial returns. However, as highlighted in recent research, the lack of standardized biodiversity metrics remains a significant barrier to scaling up such investments. Without reliable measurement tools, investors face difficulties in comparing opportunities and assessing impact.

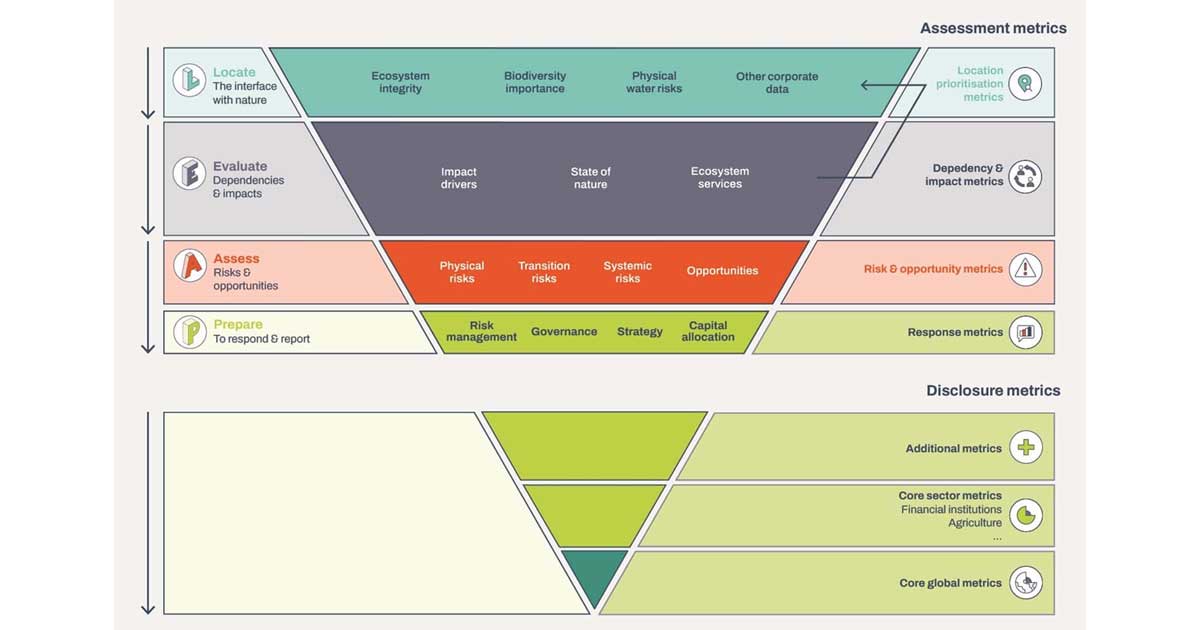

To address this challenge, various initiatives have been launched to develop common frameworks and methodologies. The Taskforce on Nature-related Financial Disclosures (TNFD) and the Science-Based Targets Network (SBTN) are among the most prominent efforts, providing guidance on how to measure and manage nature-related risks and impacts. These initiatives are expected to play a crucial role in standardizing biodiversity metrics and facilitating their integration into financial decision-making.

TNFD framework

Source: Taskforce on Nature-related Financial Disclosures. (2023).

Source: Taskforce on Nature-related Financial Disclosures. (2023).

Hungarian Applications and National Perspective

From a Hungarian perspective, the integration of nature-positive finance into national economic policy should be approached with a balanced and pragmatic mindset, ensuring that environmental objectives are aligned with economic competitiveness and national sovereignty. Hungary possesses significant natural assets, including diverse ecosystems and agricultural landscapes, which can serve as a foundation for nature-positive investments.

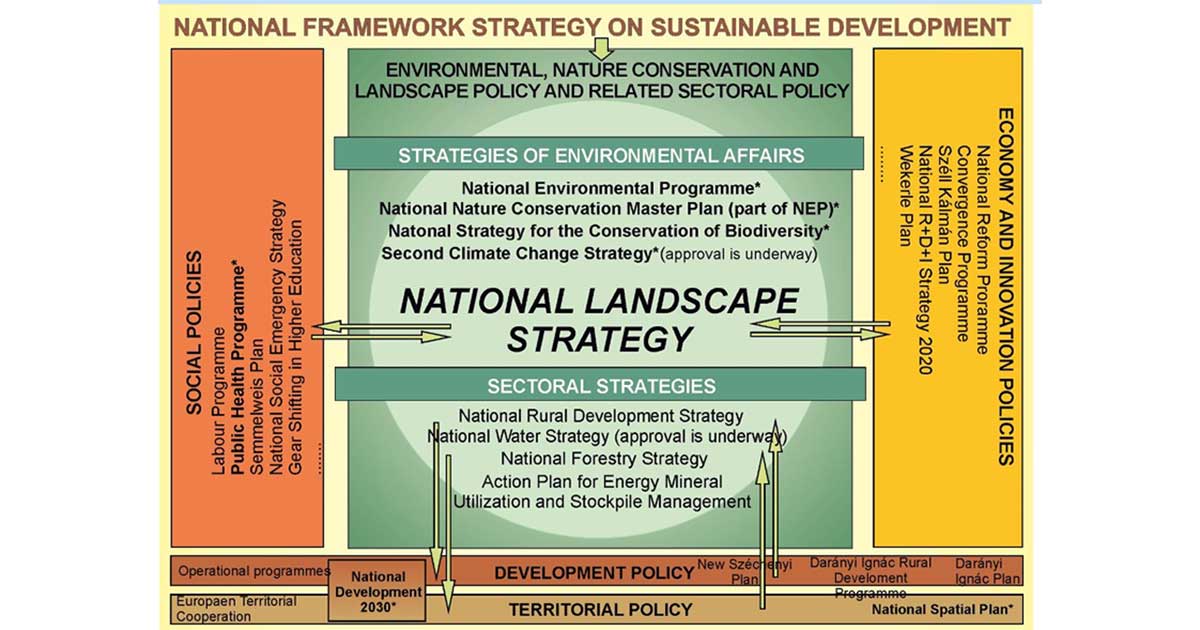

The Place and Role of the Natural Landscape Strategy within the Hungarian Planning scheme

Source: Government of Hungary. (2017). Hungarian national landscape strategy 2017-2026.

Source: Government of Hungary. (2017). Hungarian national landscape strategy 2017-2026.

The Hungarian government has consistently emphasized the importance of economic stability, energy security, and industrial development. Within this framework, biodiversity considerations should be integrated in a manner that supports domestic industries and rural communities, rather than imposing excessive regulatory burdens. For example, sustainable agricultural practices and forest management can enhance biodiversity while maintaining productivity and supporting local livelihoods.

Hungarian financial institutions, including state-supported banks and investment funds, have an opportunity to play a leading role in promoting nature-positive finance at the national level. By incorporating biodiversity metrics into lending and investment decisions, these institutions can contribute to the modernization of the Hungarian economy while aligning with EU requirements. At the same time, it is essential to ensure that such measures are implemented in a way that respects national priorities and avoids unnecessary administrative complexity.

Policy Alignment and Strategic Opportunities for Hungary

The alignment of Hungarian policies with EU biodiversity objectives should be viewed not merely as a regulatory obligation but as a strategic opportunity. By proactively engaging with nature-positive finance, Hungary can attract investment, enhance its international competitiveness, and strengthen its position within the European Union. This is particularly relevant in the context of the green transition, where access to sustainable finance is becoming increasingly important.

At the same time, Hungary must ensure that EU-level policies are adapted to national circumstances. This includes advocating for flexible implementation mechanisms and recognizing the specific characteristics of the Hungarian economy. A one-size-fits-all approach to biodiversity metrics and reporting could impose disproportionate costs on smaller enterprises and hinder economic growth.

By adopting a constructive yet cautious approach, Hungary can contribute to shaping EU policies in a way that balances environmental ambition with economic realism. This aligns with a broader conservative perspective that emphasizes gradual reform, national sovereignty, and the importance of market-based solutions.

Environmental Accounting and Green Activity-Based Costing: Advancing Nature-Positive Finance

While regulatory frameworks such as the EU Taxonomy and the TNFD provide essential top-down architecture for nature-positive finance, the practical implementation of biodiversity-informed capital allocation depends critically on the development of robust accounting methodologies capable of capturing the financial materiality of ecological processes. In this regard, environmental accounting and, more specifically, green activity-based costing (GABC) represent important yet underutilised tools for advancing the integration of nature into financial decision-making at both the corporate and institutional levels.

Environmental accounting, also referred to as green accounting or sustainability accounting, encompasses the systematic identification, measurement, and communication of the costs and benefits associated with an organisation’s impact on the natural environment. At the corporate level, it operates through three principal dimensions: environmental management accounting, which supports internal decision-making; environmental financial accounting, which generates externally oriented reports for investors and regulators; and national environmental accounting, which integrates natural resource depletion and ecosystem service flows into macroeconomic indicators such as adjusted national income and “green GDP”. The relevance of environmental accounting to nature-positive finance lies in its capacity to render visible the ecological dependencies and impacts that conventional financial accounting systematically overlooks. As the World Resources Institute has observed, nature remains largely invisible in most economic and financial decisions, not because its value is insignificant, but because it has not been treated as a critical asset necessary for the economy.

A particularly promising instrument within this broader field is green activity-based costing (GABC), which adapts the principles of activity-based costing (ABC) to the environmental domain. Traditional ABC allocates costs to products and services based on the activities that give rise to those costs, rather than relying on arbitrary overhead allocation. In an environmental context, GABC extends this logic by separately identifying environment-related costs, which can be attributed to specific cost centres, and environment-driven costs, which tend to be concealed within general overheads. By tracing environmental costs to their actual drivers, whether land use change, water consumption, emissions, or resource extraction, GABC enables organisations to understand the true environmental cost structure of their operations, products, and investment portfolios. This is directly relevant to nature-positive finance, where the accurate identification and allocation of biodiversity-related costs and benefits is a prerequisite for credible impact assessment.

The United Nations Division for Sustainable Development has identified four key management accounting techniques for the identification and allocation of environmental costs: input-output flow analysis, flow cost accounting, activity-based costing, and life cycle costing. Among these, activity-based costing has been recognised as particularly effective in making environmental costs transparent by linking them to the specific activities, processes, and products that generate them, rather than burying them in aggregated overhead accounts. Recent research has further demonstrated that integrating GABC with environmental cost accounting systems enables managers to understand not only the financial implications of environmental protection activities but also the proportion of environmental costs within overall product costs, thereby supporting more objective and accurate decision-making on biodiversity-related investments.

At the macroeconomic level, natural capital accounting provides a complementary framework for embedding biodiversity considerations into public policy and sovereign investment strategies. The United Nations System of Environmental-Economic Accounting (SEEA), and in particular its Ecosystem Accounting module (SEEA EA) adopted as a global statistical standard in 2021, offers a structured methodology for measuring ecosystem extent, condition, and the flow of ecosystem services in both physical and monetary terms. The SEEA framework is increasingly recognised as a tool that can support nature-positive finance by providing spatially explicit data on ecosystem dependencies and nature-related risks, which in turn can inform the design of green financial instruments and the evaluation of nature-based investment opportunities. As the Capitals Coalition’s 2025 roadmap for putting nature on the balance sheet has emphasised, the full integration of natural capital into financial accounting requires supportive regulation, aligned standards for measurement and valuation, and a clear pathway from value discovery to recognition in formal financial statements.

For financial institutions seeking to scale up nature-positive investments, the combination of GABC at the corporate level and SEEA-based natural capital accounting at the national level offers a comprehensive analytical toolkit. At the firm level, GABC can be applied to assess the environmental cost structure of investee companies, identify hidden biodiversity-related costs and liabilities, and evaluate the efficiency of nature-positive interventions. At the portfolio level, ecosystem service accounts derived from the SEEA framework can support the identification of nature-related risks within specific geographies and sectors, thereby informing asset allocation decisions and the pricing of biodiversity-linked financial products. Furthermore, as environmental management accounting tools such as biodiversity accounting, water management accounting, and material flow cost accounting continue to evolve, they provide increasingly granular data that can be integrated into the broader nature-positive finance architecture.

From a Hungarian perspective, the adoption of environmental accounting and GABC methods offers a pragmatic pathway for aligning national financial practices with EU biodiversity objectives while maintaining cost efficiency and administrative proportionality. Hungarian financial institutions and state-supported investment funds could benefit from integrating GABC into their due diligence and impact assessment processes, particularly in sectors such as agriculture, forestry, and water management where biodiversity dependencies and impacts are most pronounced. Similarly, Hungary’s engagement with SEEA-based ecosystem accounting at the national level could strengthen the evidence base for nature-positive policy design and attract international sustainable finance flows by demonstrating a credible and data-driven approach to natural capital management.

Challenges and Limitations

Despite the progress made in integrating biodiversity into finance, several challenges remain. The complexity of biodiversity as a concept makes it difficult to develop standardized metrics, and data availability is often limited. Additionally, the relationship between economic activities and biodiversity outcomes is highly context-dependent, requiring location-specific analysis and expertise.

Another key challenge is the potential tension between short-term financial returns and long-term environmental objectives. While nature-positive investments can generate significant benefits over time, they may require higher upfront costs or longer investment horizons. This necessitates the development of innovative financial instruments and incentives to align investor interests with biodiversity goals.

From a Hungarian standpoint, it is important to ensure that these challenges are addressed in a way that does not undermine economic stability. Policymakers should prioritize practical solutions, such as pilot projects and targeted incentives, rather than overly ambitious regulatory mandates.

Conclusion

Nature-positive finance is no longer a distant policy aspiration but an emerging reality that is reshaping the very foundations of how capital is allocated in Europe. What once stood at the margins of environmental discourse - biodiversity - is now steadily moving to the center of financial decision-making, propelled by both global necessity and the European Union’s determined regulatory agenda. Integrating biodiversity metrics into mainstream investing may be technically demanding, yet it is precisely this shift that will define whether Europe’s economic model remains viable in the decades ahead.

For Hungary, this transformation should not be viewed merely as an external obligation, but as a strategic moment to assert a distinctly national approach within a common European framework. By combining regulatory alignment with a firm commitment to economic sovereignty, Hungary can ensure that nature-positive finance strengthens rather than constrains its development trajectory. A carefully calibrated policy mix, grounded in economic resilience, innovation, and the preservation of the country’s natural heritage, can turn compliance into competitive advantage.

Looking ahead, the real test will lie in execution. Ambitions must be translated into credible metrics, transparent systems, and investment practices that deliver both ecological and economic returns. This will require disciplined cooperation between the state, the financial sector, and the real economy, without losing sight of national priorities. If managed with strategic clarity and confidence, Hungary is well positioned not only to adapt to this new financial paradigm, but to help shape it, demonstrating that environmental responsibility and national economic strength are not opposing forces, but mutually reinforcing pillars of long-term prosperity.

References

ACCA. (2023). Environmental management accounting. ACCA Global, F5 Performance Management Technical Articles.

Addison, P. F. E., et al. (2019). Biodiversity: The missing element in sustainability reporting. Conservation Biology, 33(2), 312–321.

Blanco-Zaitegi, G., et al. (2022). Biodiversity accounting and reporting: A systematic review. Accounting Forum, 46(1), 1–20.

Boiral, O. (2016). Accounting for biodiversity: Accountability and governance challenges. Journal of Business Ethics, 138(4), 761–775.

Capitals Coalition. (2025). Towards a roadmap for putting nature on the balance sheet.

Carbmee. (2026). EU Taxonomy and Regulation Guide 2026: What companies must know. Carbmee Knowledge Insights.

Choi, E., Batho, J., Rinaldi, C., Santamaria, M., Portela, R., & Moore, L. (2025). Putting nature on the balance sheet: How natural capital accounting works. World Resources Institute Technical Perspectives.

Dasgupta, P. (2021). The economics of biodiversity: The Dasgupta review. HM Treasury.

de Silva, G. C., et al. (2019). Corporate commitments to biodiversity: No net loss and net positive impact. Business Strategy and the Environment, 28(7), 1481–1495.

ESG Today. (2025). EU launches major simplification of sustainability taxonomy to ease compliance burden on companies. ESG Today.

European Commission. (2023). Taxonomy Environmental Delegated Act: Technical Screening Criteria for non-climate environmental objectives. Official Journal of the European Union.

European Commission. (2026). Commission Delegated Regulation (EU) 2026/73 amending Delegated Regulation (EU) 2021/2178 on simplification of taxonomy disclosure requirements. Official Journal of the European Union.

Finance for Biodiversity Foundation. (2023). Finance for biodiversity pledge report.

Golsteijn, L. (2022, July 17). Life cycle assessment (LCA) basics. PRé Sustainability.

Government of Hungary. (2017). Hungarian national landscape strategy 2017–2026.

Gustavsson, A. (2023, December 14). The economic imperative and opportunity in developing natural capital. Valo Ventures.

IFAC. (2005). International guidance document: Environmental management accounting. International Federation of Accountants.

IPBES. (2019). Global assessment report on biodiversity and ecosystem services.

Jasch, C. (2006). How to perform an environmental management cost assessment in one day. Journal of Cleaner Production, 14(14), 1194–1213.

Kovács, C. (2023). Leveraging impact investing in nature-positive transitions.

Lambooy, T., et al. (2018). Biodiversity and financial institutions. Journal of Sustainable Finance.

Milieu, L., ICF International, IEEP, & L. Ecosystems. (2015). Evaluation study to support the fitness check of the Birds and Habitats Directives: Draft emerging findings (p. 68).

Nature Positive. (n.d.). The Kunming-Montreal global biodiversity framework insights. Retrieved March 18, 2026.

Science Based Targets Network (SBTN). (2023). Science-based targets for nature: Initial guidance.

Swalih, M. M., et al. (2024). Environmental management accounting for strategic decision-making: A systematic literature review. Business Strategy and the Environment, 33(7).

Tsai, W-H., Lin, T., & Chou, W-C. (2010). Integrating activity-based costing and environmental cost accounting systems: A case study. International Journal of Business and Systems Research, 4(2), 186–208.

Tonnarello, F., Vermiglio, C., Migliardo, C., & Naciti, V. (2025). The impact of EU Taxonomy for Sustainable Activities on European utilities’ performance. Business Strategy and the Environment, 34, 2848–2862.

Taskforce on Nature-related Financial Disclosures (TNFD). (2022). Framework development report.

Taskforce on Nature-related Financial Disclosures (TNFD). (2023). Recommendations of the Taskforce on Nature-related Financial Disclosures.

United Nations. (2001). Environmental management accounting: Procedures and principles. United Nations Division for Sustainable Development.

United Nations. (2021). System of Environmental-Economic Accounting – Ecosystem Accounting (SEEA EA). United Nations Statistical Commission.

Vallecillo, S., et al. (2024). Greening finance and green financing need environmental metrics: The opportunities offered by natural capital accounts. Nature-Based Solutions, 6.

Weber, J-L. (2018). Environmental accounting. In Oxford Encyclopedia of Environmental Science. Oxford University Press.

World Economic Forum. (2020). The future of nature and business.